What Is the Best Loan to Build a House

How to build (and pay for) your dream habitation

Today's tight housing markets and low interest rates accept raised dwelling house prices in many areas.

Instead of competing to purchase an existing house, you might consider building a new dwelling.

There are cracking perks to building your own home: you have control over the layout and materials, you can cull the location, and there's no contest from other buyers.

Withal, financing a home construction project is more complicated than buying an existing domicile. So it'south important to empathize the procedure and costs involved before jumping in.

Check your construction loan options (Feb 21st, 2022)In this article (Skip to…)

- Nuts of edifice a house

- How construction loans work

- Structure loan costs

- Types of construction loans

- Timeline for construction loans

- Choosing a contractor

- How much can I borrow?

- Building a house vs. buying

Edifice a business firm: the basics

Building a domicile is very unlike from buying a home off the market – especially when it comes to financing the toll of construction.

A mortgage on an existing dwelling is fairly straightforward: you accept out a single loan which involves one application, on appraisal, ane closing date, and one fix of endmost costs.

With a new home construction, the process can be complicated. At that place'south not simply a mortgage to consider, only also financing for the land, labor, and materials.

If you're considering building a home, here are a few things to proceed in mind:

- Financing your dream habitation project may require a serial of loans with multiple rounds of paperwork and fees. Nonetheless, certain loan programs and lenders can consolidate this procedure

- "One–time–shut" structure loans could aid you finance the land, structure, and mortgage all with a single loan

- Expect to make a larger down payment for a construction loan than for a traditional mortgage – typically 20% to 25% (versus as fiddling as iii% for a home purchase)

- Planning is essential. The lender has to approve your builder and your construction plans along with your personal finances

- Building versus buying – Costs vary widely by location, only may exist like in many areas

If you want a custom home in your ideal location – and you take the fourth dimension and coin to make a construction loan happen – building a new house could exist a great option.

If yous're in a rush, though, yous might be better off ownership an existing property off the market.

Purchasing a home is ordinarily faster than building one, and you'll typically accept lower hurdles to clear for things like downwards payment and credit score.

Explore home loan options to build or buy (Feb 21st, 2022)How construction loans work

Building your own home could require 1, two, or even iii separate loans. For instance, y'all need financing to:

- Purchase the land

- Pay the construction costs

- Pay off the lot and construction loan with a standard mortgage, which you tin can pay off over upward to 30 years

'True' construction loans are short–term loans, ordinarily 6–18 months. They're used only to finance home construction (not the land or permanent mortgage). And in most cases, you pay involvement only on what you borrow.

Construction loan rates are usually variable interest rates based on the prime charge per unit plus a certain percentage

Some programs allow you wrap construction loan interest into the permanent financing. This can be helpful if you lot're also trying to pay an existing mortgage or rent while building your new house.

How much does a domicile construction loan cost?

Await to pay more than for construction financing than you would for a traditional home loan – even if the cost to build or purchase is virtually the aforementioned.

New home construction loans price more than for a couple reasons:

- More risk – Lenders accept on a bigger risk because the construction process includes more variables. And, the abode existence used every bit 'collateral' for the loan amount does not nonetheless be. This risk translates into higher interest rates compared to standard mortgages

- More paperwork – Money is disbursed at different points in the structure procedure, and the lender has to verify plenty work has been completed to justify the side by side "draw" of funds

Lenders besides require lien waivers proving builders have paid their subcontractors before issuing draws.

Draws tin can be washed in stages, for example, a lender might divide the project into 7 stages and release money at each stage. Or they may allow builders to request money based on the percentage of completion.

In general, the more draws allowed, the nicer it is for the architect. Still, every draw adds to your costs because of the admin work involved.

Is information technology cheaper to buy or to build a domicile?

The thought of edifice a new domicile might scare you because yous believe it's the pricier option. But, depending on location and dwelling house features, the cost of building a business firm is comparable to buying an existing dwelling house.

The average new home costs $296,652 to build, co-ordinate to the National Association of Home Builders' 2022 written report.

Real estate site Zillow reports the average price of an existing dwelling at $269,039.

Both of these numbers vary widely – by hundreds of thousands of dollars in some cases – depending on the land and specific surface area where y'all plan to buy or build.

Verify your dwelling ownership eligibility (Feb 21st, 2022)Types of structure loans

Some abode buyers use up to three separate loans to build a domicile: one loan to purchase the country, one to build the home, and ane to catechumen the structure costs into a permanent mortgage (which works like a typical home loan).

You could consolidate these steps, especially if your builder is willing to finance construction costs until y'all use a standard mortgage loan to pay off the builder.

Or, you could look for a mortgage that finances the entire procedure with one loan.

One–time–close structure loans

Some lenders offering "one–time–close" or "construction–to–permanent" loans. These are construction loans that convert to traditional mortgages after you get the certificate of occupancy for your home.

For example, Fannie Mae, FHA, VA, and USDA programs all offer 1–time close construction loans.

These mortgages require only one closing, and you get approved only in one case, alleviating the risks of two approval processes. If you go a fixed–rate mortgage, you can lock in your interest before construction begins.

For more than information, meet:

- FHA ane–time–close construction loans

- VA one–time close structure loans

- USDA one–time–close construction loans

Withal, these mortgage programs can be harder to discover from mainstream lenders, and so you should expect to shop around if y'all want one of these loans.

Getting separate loans for each stage of the construction process might be easier from a lender standpoint. It might give you more than command equally well, because you tin store for the all-time rates on each loan.

However, using 2 or 3 loans means paying two or three sets of closing costs – and going through the underwriting process multiple times.

Check your domicile loan options (Feb 21st, 2022)Fannie Mae construction–to–permanent loan

Many shoppers who prefer the "single–closing" strategy cull Fannie Mae'south construction–to–permanent loan choice.

With this program you'd make no mortgage payments while the home remains under construction. Instead, loan repayment begins subsequently closing.

Like whatever construction–to–permanent loan, Fannie Mae volition roll construction costs into your permanent mortgage once you have a certificate of occupancy.

This loan can generate "instant home equity" because Fannie Mae bases its loan–to–value ratio on construction costs, including lot conquering, assuming that number is lower than the home's eventual value.

For instance, if a home costs $200,000 to build, but an appraiser values it at $250,000, Fannie Mae would nevertheless base its LTV on the $200,000 in construction costs. You could put $twoscore,000 downwards (xx% of $200,000) and take out a $160,000 loan.

Because of the dwelling house'southward value of $250,000, you lot'd instantly have $90,000 in home disinterestedness ($250,000 minus the $160,000 loan residuum). Information technology's of import to call back structure costs and holding values vary a lot past state.

Two–fourth dimension–close loans

The other financing option is a ii–time–close construction loan – ii separate loans. Y'all'll become a construction loan first, and then repay it when construction ends by refinancing into a permanent mortgage.

This means applying for two unlike loans with two closings, and all the associated closing costs for both.

Many lenders require you to take a permanent mortgage lined up before they'll release funds for the edifice process.

This two–loan strategy gives you lot flexibility if there'southward a structure filibuster requiring y'all to extend the construction loan term.

And, you lot may have admission to better refinancing choices than with a construction–to–permanent or one–fourth dimension–shut loan.

Which structure loan is best?

The beauty of a construction–to–permanent mortgage is that you avert multiple loan applications, packages of lender fees, and championship charges.

Notwithstanding, the major drawback is that these loans lock yous in with your construction lender.

You don't ever know what mortgage rate you'll exist offered until the construction is complete. Or if you are locked in, rates may have dropped during the construction period, and y'all may be able to do better with some other lender.

Ane–time–close structure loans tin exist simpler and price less upfront, but you might terminate up with a higher mortgage rate in the long run.

Never accept your lender's permanent rate without comparison current mortgage rates from its competitors.

1–time–close mortgages tin can save money by consolidating some fees, but it's no savings if your permanent loan's interest is significantly higher than current mortgage rates.

If you lot plan to keep your domicile and mortgage for many years, information technology may pay to supercede your construction–to–permanent loan with a meliorate one. You may also be able to negotiate a lower rate with your structure lender if you bring in offers from other lenders.

Refinancing a construction loan to a mortgage loan

If you lot use a brusque–term construction loan that only covers building costs, you'll probable demand to refinance into a traditional mortgage in one case construction is consummate.

People who take out construction–but loans may exist owner–builders who plan to act as their own contractor or do the lion's share of the building themselves.

Many mortgage lenders won't piece of work with owner–builders because they can't be sure that the house will really exist a main residence and not a "spec" deal.

You might likewise choose a structure–simply loan to have more control over the permanent financing.

Y'all'd be able to shop for the everyman mortgage charge per unit in one case the dwelling becomes ready for occupation.

How to shop for a construction loan refinance

When your abode nears completion, showtime comparing mortgage rates and interviewing lenders. Don't let your credit score drop during construction, because that will increase your interest charge per unit and make blessing harder.

Merely about whatsoever program open to traditional dwelling refinances should be available to you lot every bit well. Go several quotes from competing lenders, and endeavour to get them on the aforementioned day and then you can make an effective evaluation.

Once y'all have your lender, become your awarding approved as soon as you can. Y'all'll not desire costly delays once your habitation is fix to occupy.

How long does it take to get a home construction loan?

A 90–day approval process on construction loans is common, because the lender must approve the projection and the builder, not just y'all.

Your builder should submit construction plans – including a description of materials and a price breakdown – for the lender to evaluate.

The builder's structure plans should include floor plans, ceiling heights, timetables – everything it will take to create your dream home. Experienced builders volition likely already know about your lender's requirements.

When the lender has your builder's construction plans in manus, information technology will appraise the value of the dwelling house upon its completion.

Construction loan approving often takes up to 90 days. Building the abode itself can have anywhere from 4 months to over a year.

Your lender will also evaluate your personal finances during the approving process.

For nearly programs, you need a solid credit history, a good FICO score, and a reliable income. You may take to brand loan repayments during construction. Lenders prefer you have acceptable savings for price overruns and unexpected costs.

Well-nigh lenders are helpful in this process, even providing architect approving packages.

However, approval policies, costs, and loan terms tin vary significantly. And then compare structure loan costs to see what you can afford and interview lenders advisedly before applying for loans.

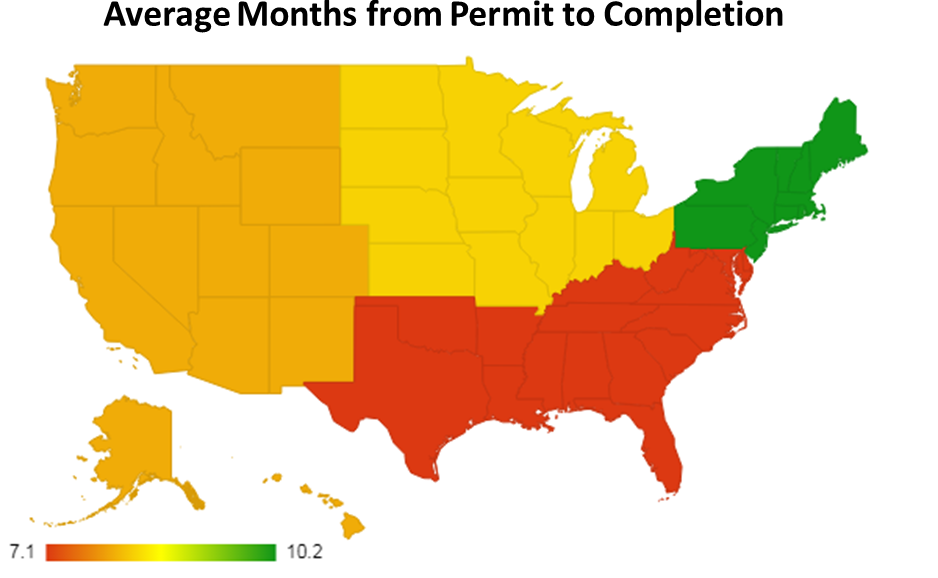

Outset your home loan approval today (Feb 21st, 2022)How long does it accept to build a habitation?

On boilerplate, it can have anywhere from 4 to 12 months to build a home.

The amount of time varies with the complication of the job, the skill of the builder, and outside forces like the conditions.

A small production home on a fraction of an acre lot might have four to six months. An enormous custom home on an acre or more takes 10–sixteen months. Labor and materials availability also influence construction completion dates.

According to the U.S. Demography, average build times also depend on your location:

Source: U.Due south. Census, Characteristics of New Housing, 2018. Image: ThePlanCollection.com

Pre–construction problems ofttimes slow projects down when clearing and prepping country reveals surprises, especially on large lots.

Permitting can also throw off your schedule and may exist a bit political. And your municipality requires y'all to get permits, code inspections, and approvals throughout construction.

The bigger the home you're constructing, the more patience and persistence you'll need.

Choosing a builder or contractor

To become financing for your dream domicile project, you'll need to piece of work with a qualified builder or general contractor.

You may accept imagined being an owner–builder, and you may have the skills to make this happen.

But in reality, you lot'd need to exist an owner–architect with deep enough pockets to finance the project yourself, because most banks won't back a do–it–yourself project.

In add-on, most lenders accept standards for builders, and if yours doesn't encounter them, you lot can't finance your construction with a mortgage lender.

This can be an reward for you – by protecting themselves from unqualified builders, lenders are besides protecting you.

How to find a qualified builder

Yous tin check your builder's licensing condition and usually find complaints by looking online for your country contractor'due south lath.

Or, just search for your prospective contractor's proper name, location, and the word "license" to get this information.

Personally interview at to the lowest degree three builders or full general contractors on your brusque listing and learn all y'all can nigh how they complete structure projects. Know whether your personalities mesh, because you'll piece of work with them almost daily for 6 months or longer.

Notation what's included and what's guaranteed (defects, overruns, and deadlines, for example).

As with any expensive contract, don't sign off on anything you don't sympathize. Get a heir-apparent's real estate agent specializing in new construction or a real estate chaser to help if you demand it.

How much can I borrow for my dwelling house edifice project?

When you're buying an existing home, it'south possible to finance up to 100% of the domicile'southward value depending on your loan program.

Non so with construction loans. Expect your lender to finance but 75% to 80% of your home'due south eventual value.

This leaves a 20% to 25% down payment requirement for you, the borrower.

Lenders crave large downwards payments because edifice your own home requires a commitment for upwardly to a twelvemonth or more. Borrowers who make a substantial down payment tend to exist less likely to walk away mid–projection.

The amount you tin can borrow afterward your downwardly payment depends on the loan program you lot use.

FHA and conventional loans take unlike maximums, and lenders may set their own limits. Then check with your lender to run across how much yous can borrow based on your loan type and finances.

Find out how much home you lot can afford

Y'all control the out–of–pocket costs for building a house past creating an affordable upkeep.

Once you know what y'all tin can spend, work with a reputable builder who knows the area and who tin can tell y'all what you can and can't beget to include in your new house.

The Mortgage Reports has a habitation affordability calculator y'all tin can employ to notice how a monthly payment translates to a loan amount, or how much abode you lot tin afford given your earnings and electric current expenses.

Begin with the basic essentials, calculation a 10% cushion for cost overruns. If yous tin afford additional amenities, add together them in.

Structure costs tin escalate, then it's smart to budget for this. For this reason, lenders often build in 5% to ten% for contingencies.

For case, if you program to spend $200,000 building, you may have to authorize for a $220,000 loan.

The architect should include a clarification of materials and a cost breakdown, which you'll need when you utilize for a structure loan.

Verify your maximum loan corporeality (Feb 21st, 2022)Building versus buying your dream home

Building versus buying is a personal choice, and your personal finances and preferences should guide y'all.

As you make up one's mind, consider these pros and cons.

Pros of buying an existing dwelling

Ownership a home can be faster and easier than building one.

You lot'll avoid unforeseen delays in the building process, and you lot don't have to pay for rent or a mortgage while waiting for your new home to be completed.

In addition, existing homes are oftentimes in established residential neighborhoods. Typically, that means they'll accept mature trees and landscaping that adds substantial dwelling value.

Mature copse and shrubbery tin also lower energy prices. In the summer, shade from alpine copse reduces cooling costs. During the winter, mature trees and shrubs decrease heating costs past blocking winds.

If you buy in a well–adult area, yous may too have civilities like shops, restaurants, and amusement within walking distance.

Cons of buying an existing dwelling house

Depending on its age, purchasing an existing domicile means buying all of its problems.

Older houses take more article of clothing and tear, are often less free energy–efficient, and tin sometimes require expensive maintenance. How much those are and when they're necessary depends on the abode'south age.

About fifty% of the average house needs replacement during its start xxx years. A house with a heating or cooling organisation, appliances, or a roof by half its useful lifespan means you'll probably cease up replacing those items.

Homeownership costs add up to thousands of dollars, depending what repairs or replacements are necessary and where yous live.

By edifice a business firm, you might not have any pregnant maintenance costs for the first 10 years. And you lot will probably have some sort of warranty protection.

Research shows that homes built after the year 2000 save their owners 21% annually on energy costs.

Verify your habitation buying eligibility (February 21st, 2022)Pros and cons of building a new dwelling

Building your dwelling puts you in control of all the decisions, big and minor, that get into a new home – from the square footage of the storage space to the height of the backyard fence.

Only there are potential pitfalls when building a new home, too. Here'south what you lot should know.

Pros of building a dwelling

Retrofitting an existing residence can get pricey. A major advantage of building new is that, from layout to location, you can tailor it to your tastes and family needs.

When you build a business firm, you can put information technology where you want it and create the environment yous need.

A new house also gets equipped with the latest features like energy–efficient materials, technology–friendly wiring, and security systems.

And you have almost complete command over the structure materials used in your business firm, as well as the price of building a home.

Your builder selection is probably the most important decision you'll make, so don't enter the relationship lightly.

That means you lot tin can make artful decisions (similar hardwood vs. carpet) too as practical decisions. For case, you might avoid toxins in the materials, making the interior environment safer for you and your family.

In add-on to making your home eco–friendly, adding Energy Star or greenish appliances makes information technology energy–efficient, reducing utility costs. You tin can cull to invest more in some areas of the house and less in others.

There are other financial benefits to building your own house, too:

- You don't pay for premium features y'all don't want, similar a finished attic or wall–to–wall carpeting

- You may get more than value for money because you get the layout you desire

- Maintenance and repair costs volition be low for the start vii to 10 years. Minor repairs go covered under your home warranty, and you unremarkably take a one– to ten–twelvemonth builder warranty

At that place aren't likely to be whatsoever unexpected negative surprises if y'all choose the right builder or contractor for your project, and go your home congenital properly.

Your builder selection is probably the most of import determination y'all'll make, and then don't enter the human relationship lightly.

Cons of building a home

Home edifice can exist complicated. It may disrupt your lifestyle.

What if the timing doesn't work out and you sell your electric current home, only have to look several more months to complete your new home? Chances are you'd have to put everything in storage and find temporary housing.

Home structure projects are prone to:

- Delays from improperly structured contracts

- Delays from changes to the construction plan

- Toll overruns

- Weather delays

- Delays because materials were delivered late

Good planning tin help avert many of these issues, simply others may happen unexpectedly.

For instance, following Hurricane Katrina, the cost of edifice materials soared – not something you'd necessarily predict.

Botched or late custom orders are non unusual. And, when a builder or subcontractor fails to follow the near recent habitation pattern, the outcome tin can be disastrous.

Every bit long every bit the mistake isn't something huge like improperly installed load–bearing walls, it'southward fixable, though not usually cost–costless.

Sometimes, builders or general contractors hide or cause construction defects. There may be home warranty problems that you don't know nearly. If your architect or domicile warranty doesn't cover these defects, yous may face large costs to correct bug.

Buying a fixer–upper: A happy medium?

One way to split the difference between buying and building is rehabbing. That is, you buy a house with a lot and foundation, and finance your renovations correct into the purchase.

You can practice this with ane of several products:

- The FHA 203(k) loan bases your loan amount on the improved value of the property and requires only 3.five% downwards for most applicants

- Fannie Mae'southward HomeStyle mortgage allows you to finance 2nd homes and rentals as well as primary residences. Put as little as 5% downwardly

- If you have depression–to–moderate income, the HomeReady loan can get you lot in the door with just iii% down and flexible underwriting

- Freddie Mac'south Renovation Mortgages are like to Fannie Mae's products. Guidelines do vary, though, so you lot might become approved for one fifty-fifty if you're declined for another

Equally with any mortgage, it pays to compare offers from multiple lenders.

Building a house: The lesser line

Homeownership has lots of advantages whether you build or purchase.

Succeeding in building your ain dwelling requires a strong squad. Your builder and your lender will exist central members of this team. They can make your dream home a reality.

Select your builder and lender carefully, and you'll have a neat chance to build the home you want within your upkeep.

Evidence me today'south rates (Feb 21st, 2022)The information contained on The Mortgage Reports website is for informational purposes only and is not an advertising for products offered by Total Beaker. The views and opinions expressed herein are those of the writer and do not reverberate the policy or position of Total Beaker, its officers, parent, or affiliates.

Source: https://themortgagereports.com/32688/complete-guide-to-building-a-house

0 Response to "What Is the Best Loan to Build a House"

Post a Comment